Back to the Future Part IV

Although we expected the stock markets to be choppy this year in our January Annual Outlook, the speed of the decline was faster than we expected. Global stock markets have reacted swiftly to expectations of rising rates with an average year-to-date1 decline of 17%, while long-term bonds have dropped 20%2. Investors are now asking what’s next with both stock and bond markets in close to bear market territory3.

Investors are anxious about rising inflation which may cause central banks to raise interest rates faster and higher. This will slow down economic growth and corporate profits and put further pressure on stock and bond markets. Raising rates without tipping the economy into a recession is a soft landing, which is a tricky balancing act for central banks. Historically, a recession was the only thing that stopped inflation. Today stock and bond markets are playing a tug of war as to when inflation will peak. No one knows when inflation will peak, but there are positive green shoots.

First, the recently announced first-quarter U.S. GDP was negative with a 1.5% contraction. Although this may seem negative at first, it’s positive from an inflation standpoint since it means the U.S. economy has slowed, which should reduce inflation. The U.S. Federal Reserve expects the second quarter to be positive at 1.8%. Thus we are not in a recession today4.

Second, the U.S. labour market remains strong, with the unemployment rate at 3.6% and job growth widespread across various industries. The unemployment rate is now back to pre-COVID levels.

Third, overall, stock markets remain attractive from a valuation and dividend yield perspective. Today dividend-paying companies with strong balance sheets and secular tailwinds are on sale for long-term investors. Today, our Matco funds are trading at a valuation discount relative to their benchmarks and higher dividend yields—an attractive entry point for long-term investors who want exposure to great companies.

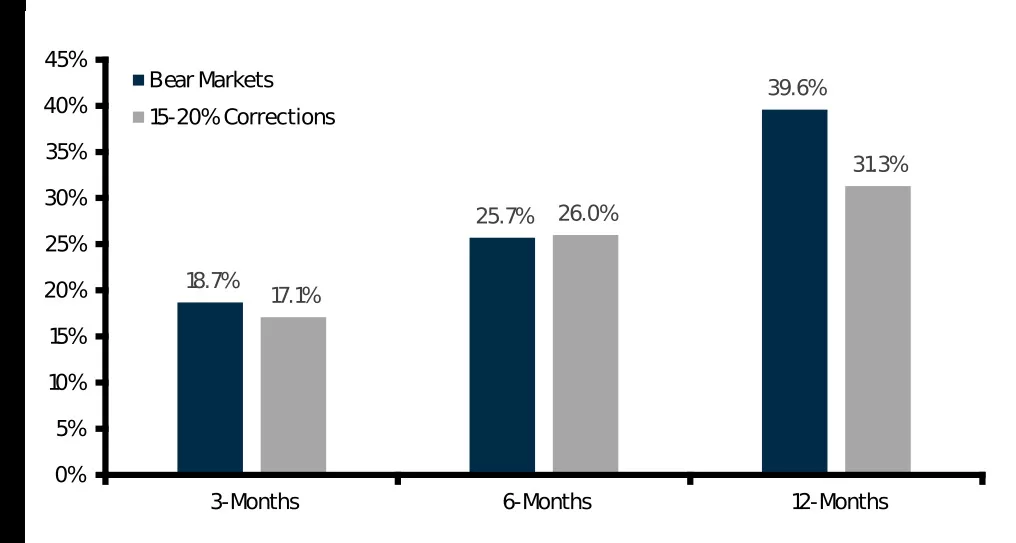

Fourth, stock markets will recover from this recession scare. We expect markets to rally when investors start anticipating that inflation has peaked. The stock market has already discounted several interest rate hikes by the central banks to battle inflation. The chart below shows that markets significantly rally over one year after corrections of 15-20%.

S&P 500 Can Register Sharp Gains After Market Price Corrections of 15-20%

Average S&P 500 Performance Following Market Corrections of 15-20%

[corrections since 1945: performance following 15-20% corrections troughs]

Source: BMO Investment Strategy Group, FactSet

The Bottom Line

Investors should stay the course with their long-term asset allocation focused on equities as the primary driver of returns. As independent money managers, we discount the headlines and focus on the underlying fundamentals. Looking back a year from now, this current market correction will be viewed as a buying opportunity.

Anil Tahiliani, MBA, CFA

Senior Portfolio Manager, Canadian Equities

Local: +1-403-539-5085

Footnotes:

1Performance as of May 24th, 2022

2Global stock market declines are measured in U.S. dollars

3A bear market is defined as a decline of 20% or more from peak to trough.

4A recession is defined as two consecutive quarters of negative GDP growth.

delivered to your inbox once a month