Bearish sentiment equals opportunity

4 minute read • September 29, 2022

4 minute read • September 29, 2022

Globally, central banks are focused on fighting inflation at all costs through aggressive interest rate hikes. Central banks are worried about runaway inflation, which they experienced in the late 1970s and early 1980s. Back then, rising inflation expectations became entrenched in the minds of consumers and businesses. The prices for commodities and everyday items spiralled upward, forcing central banks to increase rates higher than inflation, causing a major recession.

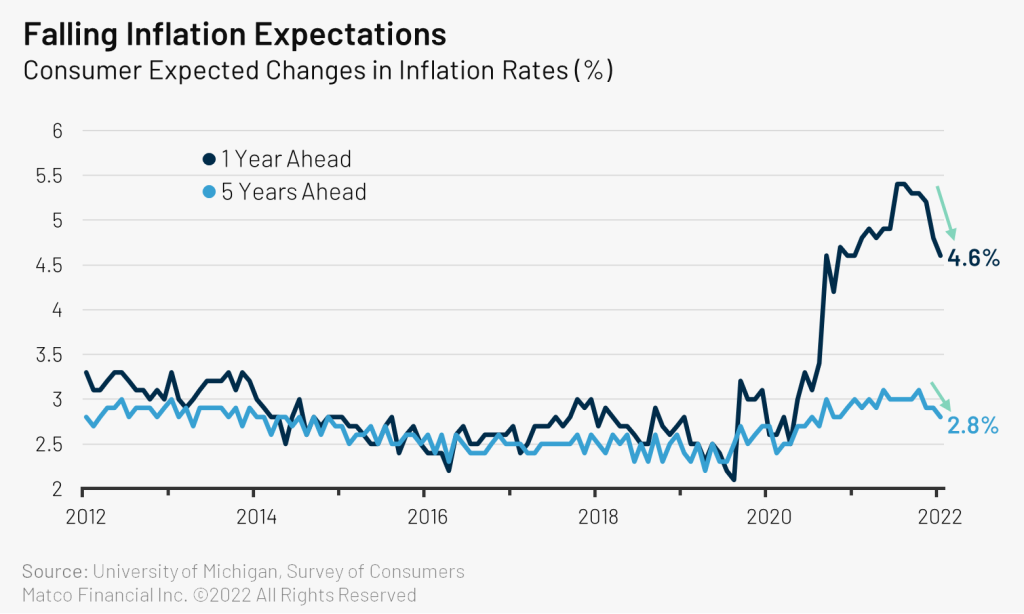

Today, U.S. consumers’ inflation expectation over the next one and five years continues to decline. Over the next year, consumers expect inflation to decline to 4.6%, while over five years, they expect it to decline to 2.8%. Thus, one could argue that the central bank’s tough talk about fighting inflation and recent rate hikes keeps future inflation expectations low. Lower expectations reduce the chances that workers will try to negotiate higher wages, which makes inflation harder to fight. Low inflation expectations are positive since central banks want to ensure that expectations do not rise significantly, which could turn into higher price inflation today.

Global stocks are in a bear market correction, with most major markets down between 15-25%. Investors are worried that inflation will lead to higher interest rates, leading to a major recession. The stock market usually leads the economy by 6 to 12 months as investors anticipate future corporate profits. Conversely, stocks rally strongly in anticipation of a recession’s end.

Economists are currently split on whether a recession will occur in the next year or whether it will be a mid-cycle economic slowdown. The wild card is when core inflation (which excludes volatile items such as food and energy costs) will peak. U.S. core inflation for August was at 6.3%, and current estimates are that it will drop to 3.7% by the fourth quarter of 2023. When the market starts seeing that core inflation has peaked, it will begin to rally on the expectation that interest rates are not headed higher.

Given the market turmoil and daily negative headlines about a recession, investors are questioning their long-term commitment to stocks.

Returns

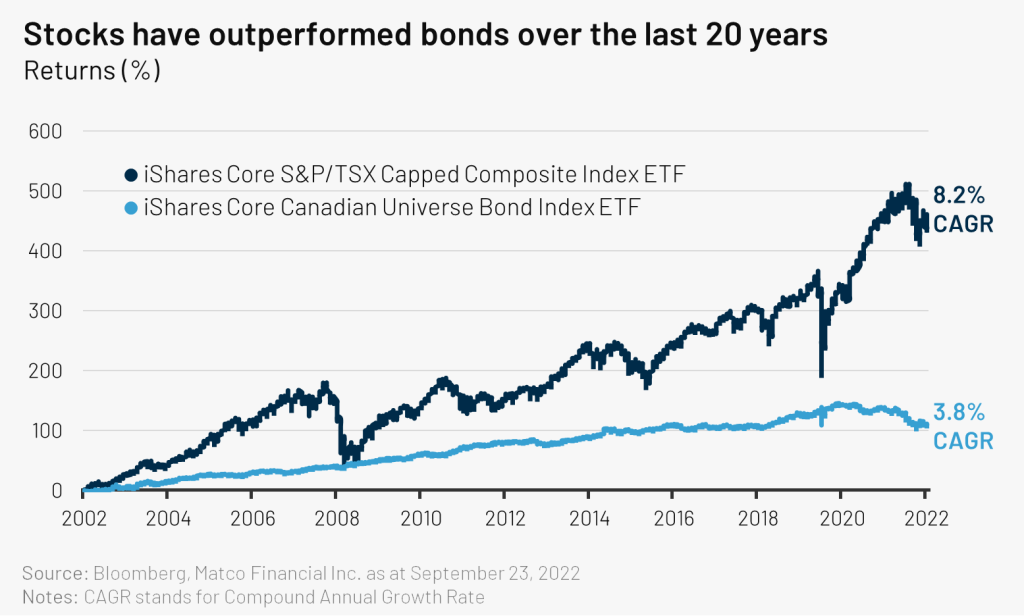

Stocks have outperformed cash and bonds over the long term. Patient investors have been significantly rewarded for owning stocks despite having higher volatility.

Income

During market corrections, investors should focus on income. Over the last two years, corporate balance sheets have been rebuilt, with many companies sitting on excess cash and having increased dividends or paid special dividends. We expect this trend to continue. Our funds focus on dividend-paying companies that generate excess free cash flow and have strong balance sheets. Our funds have the following dividend yields1:

The yields of our funds are equal to or higher than their benchmarks2.

Valuation

During every market correction, companies with high valuations fall more as investors reset earnings expectations, as seen in the technology sector. This correction has not been any different, with the global technology sector down 31% year to date3. Our M-Factor investment process guided us to sell most of our technology exposure last December, allowing our funds to exhibit good downside protection in these volatile markets.

Warren Buffet says, “Price is what you pay; value is what you get. Whether we’re talking about socks or stocks, I like buying quality merchandise when it’s marked down.” The market correction has put high-quality dividend-paying companies on sale — especially the ones we own in our funds. Matco’s equity investment funds have lower valuation multiples than the broader market as a result of our investment process. Our investment process allows us to identify and invest in dividend-paying companies with solid balance sheets. Dividend-paying companies often can repurchase shares, increase dividends while growing their business, or both.

Markets go through turbulent times, and it’s essential for investors to re-visit their objectives and ensure their portfolio aligns with their risk profile. When fear builds in the marketplace, it often represents an opportunity to deploy additional capital into an investor’s portfolio if money is available. It also represents a good opportunity for investors to rebalance their target asset mix.

Matco’s M-Factor investment process has been specifically designed to manage investment portfolios through all market landscapes. Our focus on risk management and downside protection has allowed us to develop long-term track records that our investors rely on.

Footnotes:

1Matco Fund Divided Yields as at August 30th, 2022

2 CPMS, Morningstar as at August 30th, 2022

3 iShares Global Tech ETF as at September 28th, 2022

delivered to your inbox once a month