Silicon Valley Bank fallout

5 minute read • March 20, 2023

5 minute read • March 20, 2023

Silicon Valley Bank (SVB Financial Group or SVB) was the 16th largest bank in the United States and the first notable financial institution to be put into regulatory control and receivership since the financial crisis of 2008. SVB has captured financial media coverage and is likely to receive additional coverage in the coming weeks, but it’s not the first bank to enter receivership since 2008.

On October 23, 2020, the Almena State Bank, Almena, Kansas, was closed and followed a similar process—but there was hardly any coverage of that banking collapse partially due to its size.

Broad markets and the finance sector in the United States and Canada have experienced a sell-off of their stock values due to the fear of other institutions being drawn into the collapse.

Matco Global Equity Fund does not have direct exposure to the stock of SVB, nor does Matco Financial hold any fixed-income securities issued by SVB.

In the simplest explanation, banks take in deposits and then make loans to personal or commercial borrowers. For a bank to exist profitably, the institution lends money at a higher rate than it pays depositors. Earlier this year, SVB began to feel the pressure of a higher interest rate environment brought on by central banks trying to cool inflation.

In practical terms, higher rates mean that banks like SVB must increase the interest rate with which they pay depositors to keep their deposits or attract new depositors. At the same time, the bank must invest those deposits into assets at higher rates. When a depositor pulls money from the bank, the bank may need to raise capital by selling an asset or using cash on hand.

As rates rose in 2022, the assets SVB held on its balance sheet decreased in value and presented a capital deficiency for the bank, where it owed more in deposits than it had in liquid assets.

The problem for SVB is that they had a very focused customer base, which consisted mostly of early-stage technology companies and their employees. With higher wages and a challenging business environment, these tech firms are still trying to grow into profitable businesses, drawing on their deposits more quickly.

Think back to 2019 to 2021, when many of these start-ups raised significant capital. Well, they deposited this capital with SVB, which bought assets or made loans at the current market interest rate. Now that rates have risen, these securities aren’t worth the same amount, and SVB needed to raise capital to meet its deposit obligations.

On March 9, 2023, SVB stock had declined by 60.4%1, cementing the dire situation and raising capital to shore up the bank extremely difficult. While the issuance of equity was in the process, it was too little too late, and the regulators stepped in to take control of the bank’s assets and deposits.

What’s next?

The Federal Deposit Insurance Corporation (FDIC) has taken control of both the deposits and assets of SVB. In the United States, the Federal Deposit Insurance Act insures deposits up to $250,000 per depositor for each account ownership based on FDIC’s category, which protects these small deposits from this type of business collapse.

We understand that depositors of SVB with balances of up to $250,000 will have access to their money on March 13, and banking activities will resume as normal. For depositors with more than 250,000 in their bank account, the FDIC, the Federal Reserve, and the government of the United States enacted reforms to protect these additional deposits and restore confidence in the U.S. banking system by insuring all deposits held at the bank.

U.S. banks regularly pay into a pool of capital for these types of scenarios, and as a result, the U.S. taxpayer will not be asked to pay for this bank collapse at this time.

Matco Financial’s investment philosophy consists of a systematic process guided by our M-factor model for screening equities based on their fundamentals and profitability. This process constructs a portfolio that is well-diversified and able to keep up in good markets while protecting capital in down markets.

These fundamental factors have pushed us away from owning bank stocks and directed us to more industrial, consumer discretionary, and service-based businesses in the United States. Further, our geographic diversification within global equity means the U.S. market makes up 60% of the fund’s geographic exposure while the rest of the world makes up the remainder.

Figure 1: Global Equity Fund Performance (see disclaimer)

Peer group rank is based on Global Equity Managers in Canada, with a lower number being a higher performer.

Source: Morningstar, Matco Financial Inc., as at March 10, 2023.

Using fundamental analysis, the M-factor helps us to select securities using nine specific factors focused on a company’s profitability, value, and risk. Using these factors, we rank companies in the universe and complement this ranking with research from other sources.

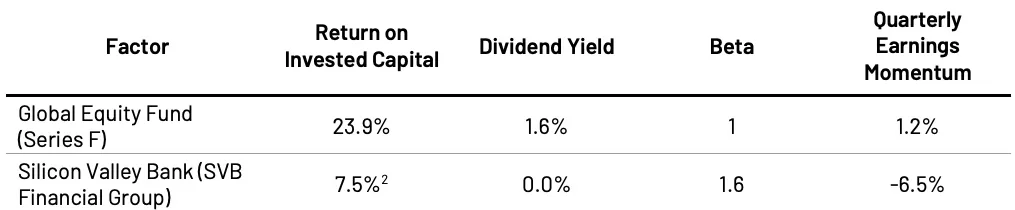

Our process targets companies with consistent earnings growth, strong profitability, and reasonable market risk. Below is a table of some Global Equity Fund factors compared to SVB.

Figure 2: Global Equity Fund Performance

2Return on equity is used for financial institutions vs. Return on Invested Capital due to the nature of the banking business.

Source: Morningstar CPMS, Matco Financial Inc., as at March 10, 2023.

As you can see by the table, SVB would not add value to any of the factors above and, as a result, was not included in our buying universe.

To be successful investors, we need to be compensated for the risk we are taking. With a beta of 1.6 vs. the S&P 500 and poor profitability ratios, SVB wouldn’t make the cut. There wasn’t enough compensation in the form of a dividend yield, in their return on invested capital, or quarterly earnings momentum to suggest that the stock would provide upside in the long run.

By sticking to our investment process, the intra-year weakness in the U.S. market presents an opportunity for us to continue to look for financially healthy businesses with a compelling value proposition. By investing with discipline and a fundamental focus, we help our clients navigate the investment landscape over market cycles to create long-term value.

1As per FactSet, March 10, 2023

Disclaimer:

The Fund returns are calculated and reported in Canadian dollars and are historical simple returns for the YTD and 1-year periods and annualized compounded total returns for periods after 1 year. They include changes in unit value and reinvestment of all distributions and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any security holder that would have reduced returns. Matco Fund returns are calculated after management fees and operating expenses have been deducted.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the Fund Facts and Prospectus before investing. Mutual funds are not guaranteed, their values change frequently, and past performance is not indicative of future performance. Matco Funds are not available for purchase in Quebec or Newfoundland & Labrador.

delivered to your inbox once a month