Central Banks Are Having Their Cake And Eating It Too

February 29, 2024

February 29, 2024

Key Points

As you may recall, our annual outlook for this year included three possible scenarios: a soft landing, a turbulent landing, and a crash landing. We put the largest probability on the turbulent landing scenario.

Although the soft-landing scenario would be the most appealing for investors, central banks and all stakeholders involved, we thought now would be a good time to highlight the risks that led us to put the greatest probability on the turbulent landing scenario: debt.

Let’s be clear: the intent isn’t to suggest a doomsday scenario on the horizon. Rather, we would like to highlight the tug-of-war global central banks grapple with. As you might have guessed, this tug-of-war concerns whether international central banks can proverbially “have their cake and eat it too.”

Having their cake: leave interest rates elevated. Why? So, inflation comes down to levels within their long-term target of 1% to 3%, coupled with a reduced risk of causing a second wave of inflation.

Eating it too: Having the economy continue to grow at a healthy pace, without unemployment drifting higher and without commercial and personal loan defaults rising.

Most of the discussions I have with investors and prospective investors surrounding debt gravitate toward government debt. It isn’t surprising as government spending has reached levels that seem reckless. We can debate whether government debt levels will become a problem, but I’m more inclined to discuss that issue on a much longer horizon, say 10 to 20 years.

Unfortunately, governments have more flexibility in dealing with debt problems. Rating agencies are slow to adjust sovereign credit ratings, debt levels can be inflated away or forgiven, and government budgets are flexible and, if need be, can be expanded to include higher debt service costs. Corporations and consumers, unfortunately, don’t have access to the same flexibility or money printing presses that governments do. They’re subject to their respective balance sheets. If we look at the consumer base, their marginal consumption capacity hinges on two primary factors: increasing marginal employment and leverage (debt). With unemployment rates at very low levels, there is little room for additional employment earnings to propel growth and consumption.

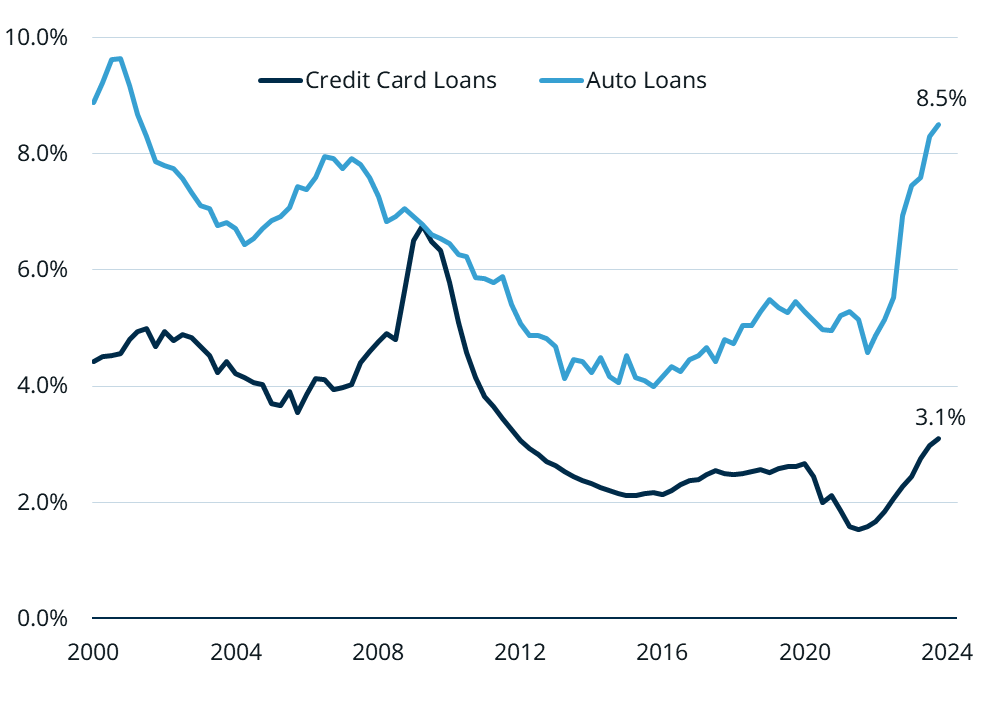

With financial institutions tightening lending standards due to rising consumer loan delinquencies, their capacity to propel growth through additional borrowed money is also limited. Over the last 12 months, credit card delinquencies have risen while banks have been tightening lending standards. Although the levels are still reasonable and not alarming, they indicate that consumers may begin to reign in spending and will be more reliant on their current income levels to pay down debt and fund their consumption.

Auto Loan and Credit Card Delinquencies

Source: FRED Graph Observations, Matco Financial Inc. as at February 28, 2024

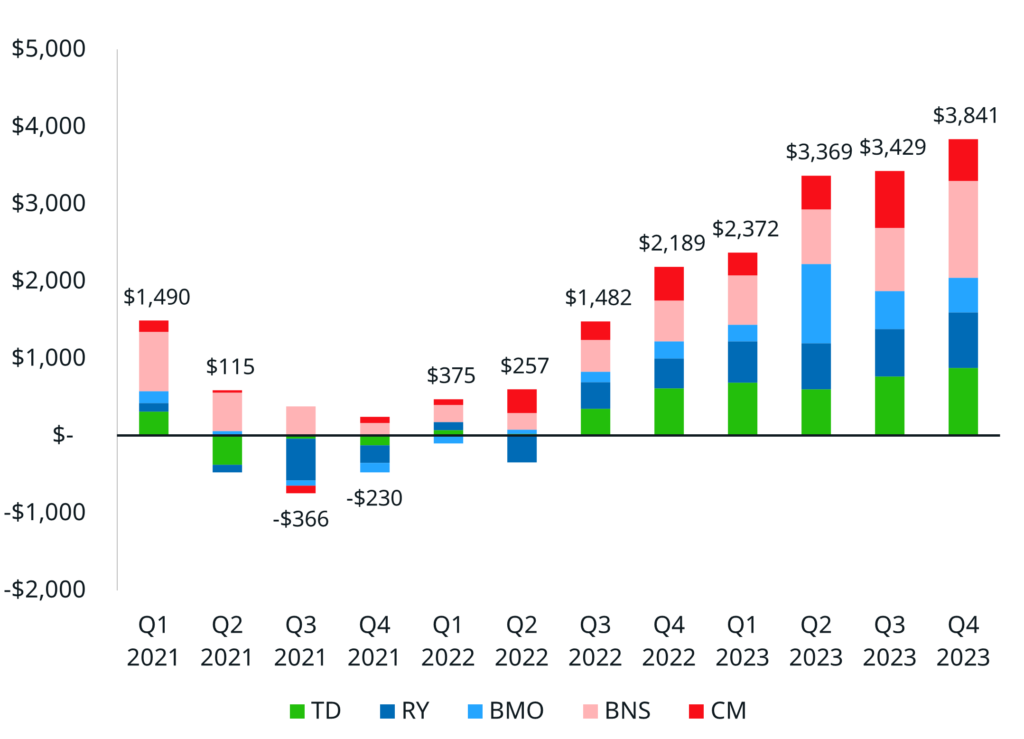

Banks’ tightening of lending standards can be highlighted by looking at the recent trend in what’s referred to as “Loan loss provisions.” These fancy words mean banks have begun preparing to write off loans because either corporations or consumers will have difficulty repaying them. Banks prematurely write off loans today that they expect not to be repaid in the future.

Given the recent rise in loan loss provisions, it isn’t surprising that they aren’t that eager to lend more money in the current environment. Again, these loan loss provisions include corporations and consumers combined, so they don’t specifically highlight the weakest area.

Provisions for Credit Losses

Source: Bloomberg, Matco Financial Inc. as at February 28, 2024

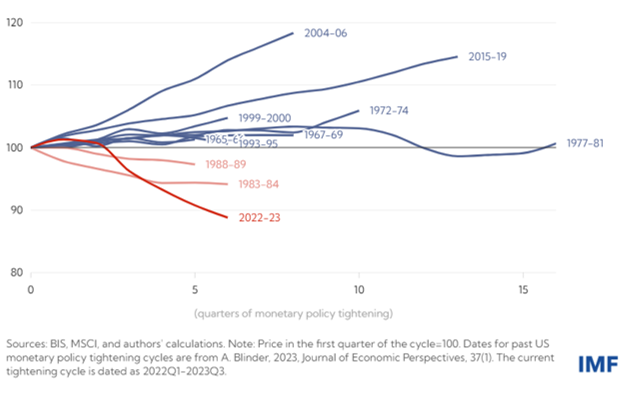

The last area to highlight is the commercial real estate market, particularly in the U.S. Debt is the engine that keeps commercial real estate markets running smoothly. What allows the cylinders of this engine to keep firing are stable property values, access to credit (or loans) and increasing demand. Unfortunately, all three of these cylinders are facing uncertainty.

Commercial property values in the U.S. have declined 11% since the beginning of 2022. Not surprisingly, this is when the Federal Reserve began dramatically increasing interest rates. 11% is not an alarming level of decline.

As previously mentioned, with banks increasing their provisions for credit losses, they are tightening their lending standards, making it more difficult for existing owners and new purchasers of commercial real estate to access credit.

Lastly, although previously mentioned, with banks increasing their provisions for credit losses, they are tightening their lending standards, making it more difficult for existing owners and new purchasers. Actual change will last forever, but the demand cylinder hasn’t fully recovered since the COVID-19 pandemic. Combined with these pressures, commercial real estate isn’t firing on all cylinders.

US Real Commercial Real Estate Prices During Monetary Policy Tightening Cycles, Index

To state the obvious, the future is unknown. If central banks leave interest rates elevated, consumer and corporate debt loads are more likely to become a problem for the economy. If they reduce interest rates, they may avoid the debt problem, contain inflation, and allow smooth economic growth to prevail. If this sounds like a difficult task, we’re on the same page.

Investors favour a smooth transition from higher borrowing costs to lower interest rates. The immaculate soft-landing scenario has increasingly become a consensus in early 2024. We’re not dissimilar from consensus because we hope this scenario plays out. However, as we often say at Matco, hope is not a good strategy. Our preference and discipline are to understand the risks and opportunities ahead.

The increasing risk of debt becoming a problem for economic growth is why we favour protection rather than growth in the Matco Balanced Fund. It means we have increased our hedge to downside risks by increasing our exposure to conservative fixed-income assets while reducing our equity market exposure. It will provide our investors with greater downside protection, allowing them to capitalize to a greater extent on lower stock prices if these risks surface.

If central banks pull off the immaculate soft-landing scenario, there will be an opportunity cost to our more conservative portfolio. However, with history as a guide, we know that central banks have executed poorly when transitioning from higher interest rates to lower ones. For this reason, we struggle to believe in a scenario where they will have their cake and eat it, too. Matco’s Balanced Fund is going to pass on the desert for now.

delivered to your inbox once a month