Central Banks Set the Stage for Lower Rates

February 9, 2024

February 9, 2024

The Bank of Canada held their most recent policy meeting last week, while the Federal Reserve concluded its Federal Open Market Committee (FOMC) meeting on January 31st. Both central banks left their overnight interest rates unchanged. Both central bank chairs reiterated the significant progress that has been made in reducing the rate of inflation.

While the Canadian economy has slowed materially to a 1.0% annualized GDP growth rate, the U.S. economy has shown more resilience with an annualized GDP growth rate of 3.3%. At the Federal Reserve’s post-meeting press conference, chair Jerome Powell snuffed out the market’s recently ignited expectation that they would begin their interest rate-cutting cycle in March.

“Based on the meeting today, I would tell you that I don’t think it’s likely that the committee will reach a level of confidence by the time of the March meeting.”

–Federal Reserve Chair Jerome Powell

Nonetheless, he further confirmed the high probability they will cut rates later this year.

“We believe that our policy rate is likely at its peak for this tightening cycle and that, if the economy evolves broadly as expected, it will likely be appropriate to begin dialling back policy restraint at some point this year.”

–Federal Reserve Chair Jerome Powell

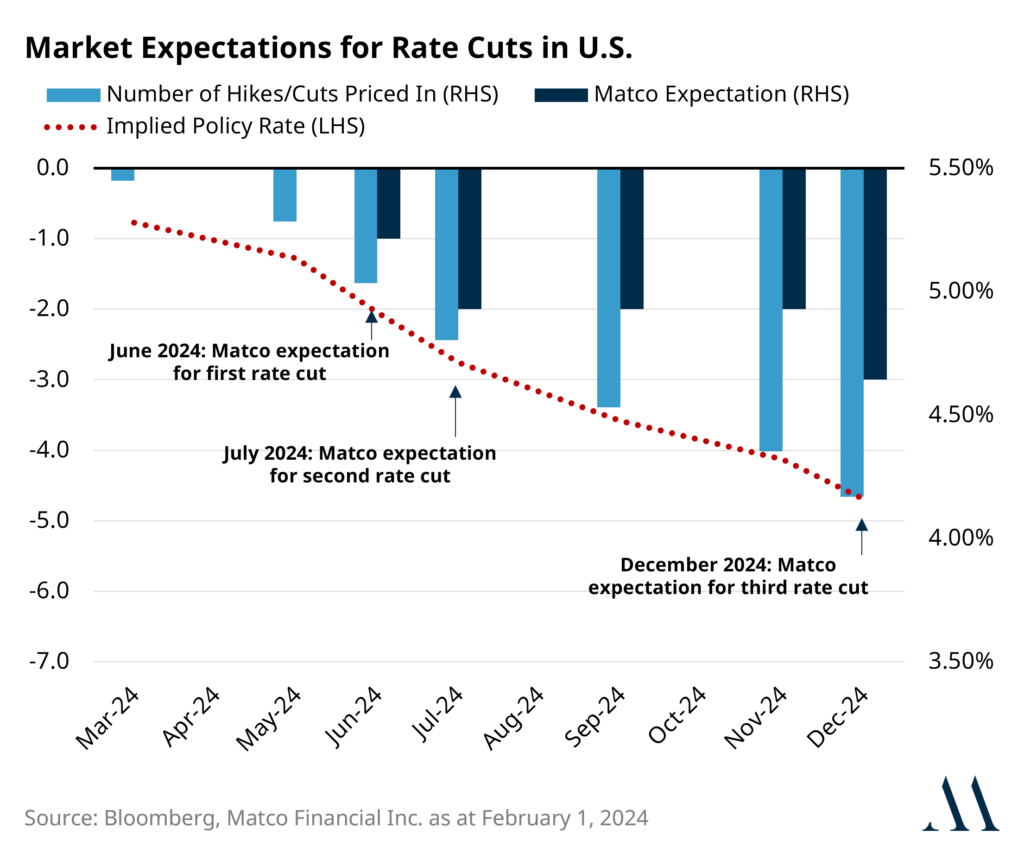

The Bank of Canada’s post-meeting statement, press conference, and the rhetoric received from the Federal Reserve have reaffirmed our current interest rate expectations for this year. Matco anticipates 3 to 4 interest rate cuts of 0.25% each from both banks throughout 2024. It means Canada’s overnight rate, which started at 5.0%, would finish the year between 4.25% and 4.00%.

Similarly, the U.S. overnight interest rate, which began at 5.5%, would finish the year between 4.75% and 4.5%.

Our view is that the first interest rate cut will occur sometime around mid-year, with two cuts likely before the U.S. election, perhaps a pause for the political process to run its course before resuming with a third and potentially fourth cut post-election. The Bank of Canada will likely begin earlier but follow a similar path.

Finer details aside, what’s most critical is that the economy is evolving to allow both central banks to begin easing financial conditions. It means that the path of least resistance for interest rates is lower by year-end. Certainly, the path will not be a straight line; nonetheless, a downward trajectory for interest rates is a positive for the bond market and investors with fixed-income exposure in their overall portfolio.

The Matco Investment Management Team will steadfastly observe as economic data unfolds and we progress closer to the central bank rate easing cycles. Active fixed-income portfolio management is critical during the inflection point of central bank activity, pivoting from a tightening bias, increasing interest rates, to an easing bias, decreasing interest rates.

We will monitor and re-position the duration and curve exposures, terms of bonds we hold short, mid, and long, within the Matco Fixed Income Fund to maximize our investors’ income and capital appreciation efficiency.

delivered to your inbox once a month