Federal Reserve Meeting: Don’t Go Chasing Waterfalls

4 minute read • December 12, 2023

4 minute read • December 12, 2023

Although the stock market always gets more attention than the bond market, the last six weeks in the bond market have been a tidal wave, or perhaps a waterfall would be a more appropriate description.

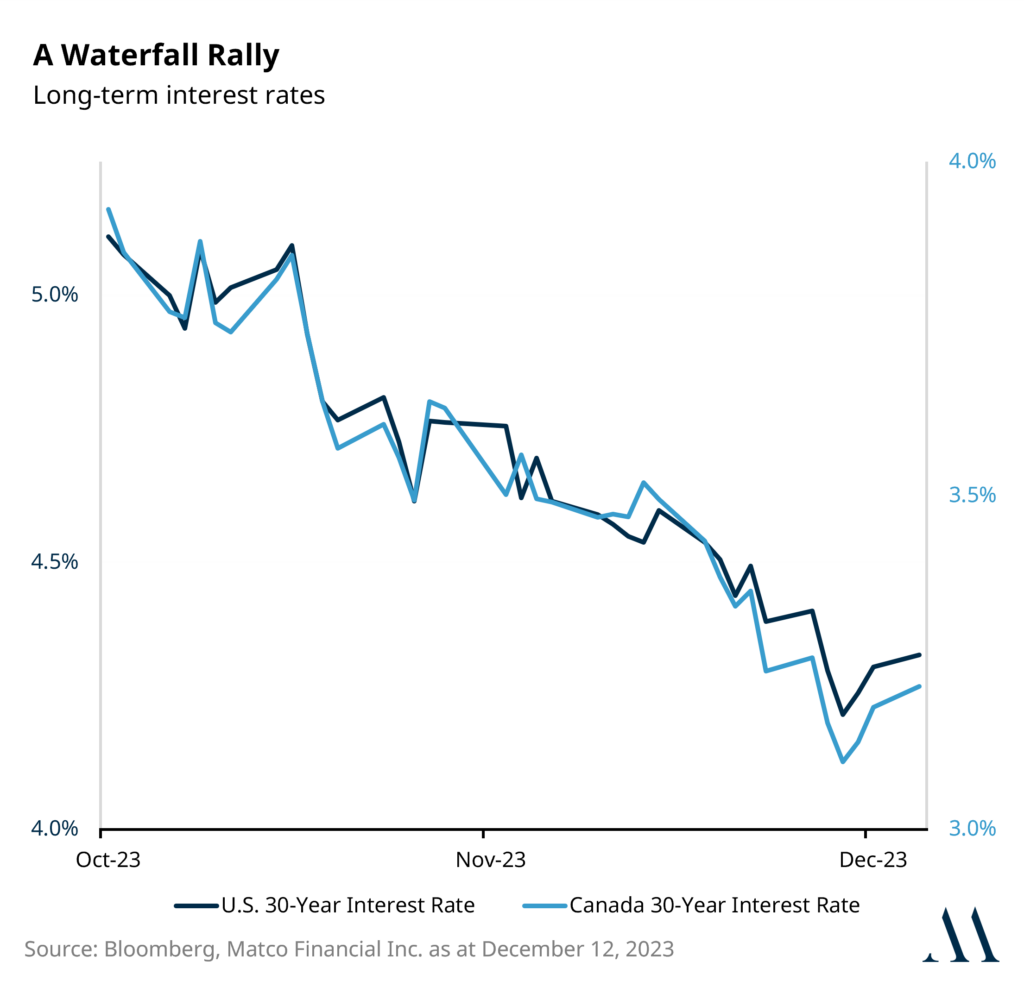

If we use the 30-year interest rate as a proxy, Canadian and U.S. interest rates peaked in mid-October at 4.0% and 5.1%, respectively. As discussed in my recent market insight, Fixed Income: The Swap Market vs. The Fed, the tide was poised to shift, and it did.

Since mid-October, interest rates have rallied (moved lower) by 0.9% in 6 weeks. Looking at a chart of the 30-year interest rate, it has been a “waterfall rally.” In the market, this means a one-way direction with very little pause.

Often, the cause of a waterfall rally is an inflection point (change of direction) combined with investors being caught off-side and having to cover their short positions or “chase the rally.” For those already in the boat, this is a great thing. For those who are not in the boat, they’re left chasing the waterfall, building further momentum and a significant rally.

Having managed assets in the bond market for 15 years allows me to put this market move into context. A 0.90% move lower over six months is significant, let alone six weeks. Through this short period, Canadian 10-year bonds were up 8.5%, and Canadian 30-year bonds were up 21.2%.

This rally was fast and furious, which begs the question, what caused such a tidal shift? Enter stage left: the swap market.

The swap market is an exchange that, among other things, communicates to market participants the expectation for future monetary policy. More simply, it indicates whether investors are expecting central banks to increase or decrease their overnight interest rates in the future.

Earlier this year, the swap market was forecasting one interest rate cut for 2024, a 0.25% rate decrease. A recent softening of economic data altered this landscape, and it happened quickly. By mid-October, the swap market was forecasting four interest rate cuts by the end of 2024, a 1.0% rate decrease. The swap market was indeed the river that led to the falls.

Although TLC made it clear in 1994 that chasing waterfalls is a bad idea, investors were forced to reposition their portfolios into longer-term bonds so they didn’t miss out on the rally.

On the other hand, Matco’s Fixed Income Fund spent most of 2023, increasing its duration position by 1.6 years, leaving us 0.6 years long versus the Canadian Fixed Income benchmark before the rally began. Our investment management team has been proactively positioning our strategies for decelerating growth, extending duration being an important piece of this positioning.

The U.S. Federal Reserve will conclude its next rate decision meeting today. Jerome Powell, Fed chair, has consistently communicated that interest rates will be “higher for longer.”

In our recent market insight, Fixed Income: The Swap Market vs. The Fed, we were vocal that this phrase was used as a defence mechanism to avoid further growth deceleration. Powell’s “higher for longer” message was an attempt to build a dam for this type of waterfall rally before it happened.

Although we believe the swap market is a more accurate forecast of the Fed’s rate decisions, at the time of writing that market insight, it was far less stretched than it is now. Even if the Fed needs to cut rates next year, the swap market might indicate too many cuts too quickly.

The Federal Reserve is aware of the swap market and the recent rally in the bond market. Given their concern that lower interest rates (borrowing costs) may risk their progress in bringing down inflation, Jerome Powell is likely to double down on his “higher for longer” communication.

It would be a nudge that the bond and swap markets might get ahead of themselves, damming the rally.

Frankly, we would agree.

Although we believe interest rate cuts will happen in 2024, the Canadian and U.S. central banks will do so cautiously. As a result, longer-term interest rates will also be lower, but they won’t arrive at the destination in a straight line or straight down the waterfall.

From a portfolio positioning perspective, thankfully, we didn’t have to chase the waterfall. We rode down the falls in our long-duration position smoothly, benefiting from the capital appreciation of the long bonds in our portfolio.

Looking out to next year, we will remain in a long duration until the rate cuts have come and gone. However, given how rapid the rally has been, moderating this position will allow us to take advantage once the interest rate kayak bounces off the pool at the base of the cliff.

If Powell does indeed walk back the swap market from its current aggressive stance, this will create another entry point of higher yields and lower prices for longer-term bonds.

It’s worth noting that our focus within Matco’s Fixed Income Fund is always long-term and far more strategic than tactical. Certain instances may lead to risk management adjustments.

With the current risk being an overstretched bond market and interest rates having moved too low too quickly, it’s worth taking some profits while allowing interest rates to re-calibrate to a more reasonable level heading into 2024.

delivered to your inbox once a month