Fixed Income: Get on the Ship Before it Sets Sail

March 12, 2024

March 12, 2024

Positioning an investment portfolio is best done proactively before anticipated developments. If anticipation is not part of the equation, then the ship of investment returns the investor is seeking to benefit from will have left the port and sailed into the sunset.

This is a very relevant consideration today for the Canadian fixed-income landscape and those currently invested in GICs. With interest rates having normalized, Matco’s Fixed Income Fund now offers current yield (income over the next 12 months) and yield to maturity (income over the longer term) greater than 4%. This rate is the most attractive it has been in the last five years, allowing investors in the Fund to benefit from a healthy stream of income. In addition, if interest rates move lower, the Fund stands to benefit from capital appreciation, which also benefits investors.

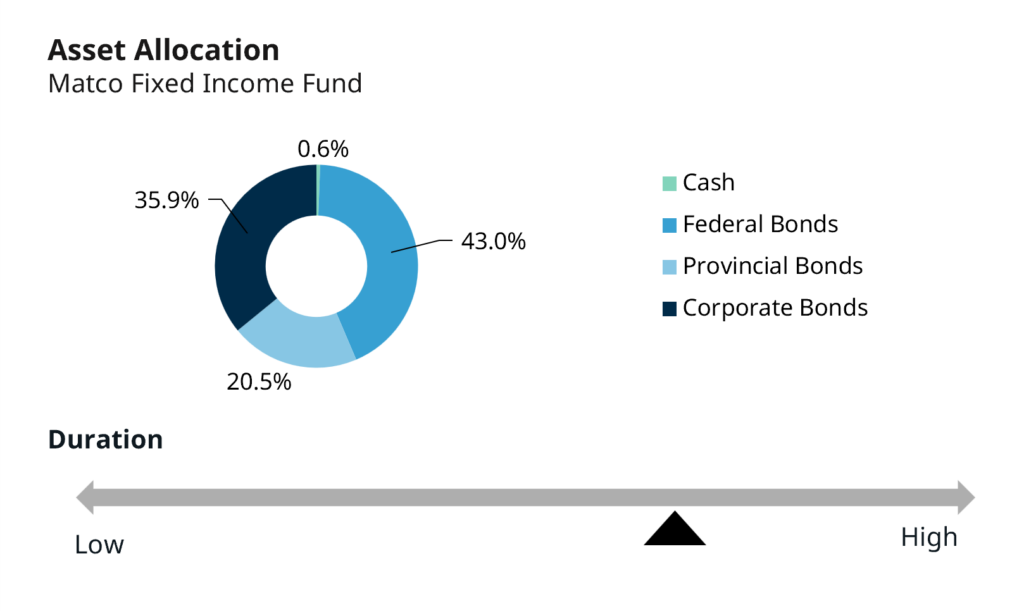

Portfolio Positioning:

| Assets Under Management | $121MM |

| Duration | 7.6 Years |

| Current Yield | 4.07% |

| Yield to Maturity | 4.04% |

| Average Credit Rating | AA |

| Number of Holdings | 30 |

Source: Matco Financial as at March 6, 2024

This positioning has been gradually put in place over the last 12 months in anticipation of rates moving lower over the next 12 months. Positioning longer term and longer duration needs to be done before the Bank of Canada begins lowering the overnight interest rate. The underweight in the corporate bond sector also needs to be in place before economic deceleration reaches a trough and creditors tighten lending standards, making it more difficult for corporations to refinance their debt.

Regarding our outlook and portfolio positioning, the Bank of Canada released their rate announcement on March 6, leaving its overnight interest rate unchanged for the fifth consecutive meeting. Although they are not yet prepared to begin cutting rates, doing so is likely to begin later this year. Bank of Canada Governor Tiff Macklem reiterated that they would like to see further progress in bringing inflation closer to their 2% target.

“We don’t want to keep monetary policy this restrictive longer than we have to,” Macklem said, articulating his desire to begin lowering rates. “But nor do we want to jeopardize the progress we’ve made in bringing down inflation.” This highlights that they understand rates will need to be lowered, but they will do so cautiously and be more comfortable when the decision is further reinforced by economic data.

Exactly when the Bank of Canada begins lowering the overnight rate is a well-covered debate. We’re less concerned with the timing and more concerned with our portfolio being positioned before it takes place. The period the Bank of Canada and the U.S. Federal Reserve wait to decrease rates will likely impact the pace of doing so. Wait longer; rate cuts may need to be more aggressive. Wait less time; rate cuts may be more gradual.

The Bank of Canada is closely monitoring inflation, so let’s dive in a little. The largest contributor to inflation remaining sticky on its downward descent is elevated shelter prices. This begs the question, is the Bank of Canada expecting the wake in the water to lead the boat? The calculation for shelter, which is included in CPI (Consumer Price Index), includes mortgage interest costs, property taxes, insurance premiums, maintenance, and repairs. Elevated mortgage rates are contributing to elevated shelter prices and, therefore, CPI. Yet higher mortgage rates are unlikely to come down until the Bank of Canada begins lowering the overnight rate. Herein lies the conundrum. To an extent, they’re waiting for shelter prices to come down, knowing their rate cut will ultimately allow CPI to come down. The longer they wait for inflation to cool, the larger the percentage of consumers that will be forced to renew their mortgages at higher rates. This would only put further pressure on the consumer’s ability to continue supporting the economy through discretionary spending.

All things considered, the Canadian economy is growing sluggishly and decelerating. Lower interest rates will alleviate some of this pressure by supporting the current rate of consumption while also supporting corporate and personal debt refinancing. Investors currently invested in GICs will be faced with lower interest rates and forced to reinvest at lower rates in the future. Meanwhile, a properly positioned fixed-income portfolio is currently offering healthy income and a potential capital windfall if rates move lower. The fixed income landscape is offering investors a larger opportunity set for their portfolios. Those invested in GICs may be left on shore wishing they had boarded the ship.

delivered to your inbox once a month