Four takeaways from 2022 for investors

8 min read • January 11, 2023

8 min read • January 11, 2023

Although Russia’s invasion was telegraphed months in advance, most investors never thought Russia would invade a Western-allied democratic country. Russia correctly bet the West would not risk a full-on military conflict with a nuclear superpower to prevent an invasion. Market reaction was swift, with stocks and bonds sharply selling off while oil, gas, and food input prices rose significantly, adding to global inflation concerns.

While news headlines focused on the invasion for the next six months, another conflict was brewing—an economic one in Asia.

Rising dragon

The conflict brewing was China’s desire to be an economic, military, and geopolitical competitor to the United States and become a leading global influence. The United States-China relationship is at an all-time low and is not likely to get better regardless of which party controls the U.S. Presidency. The Trump and Biden administrations have taken a hardline with China due to trade tensions, recent indirect support for Russia’s invasion and their desire to have Taiwan rejoin China (including by force if necessary). In addition, China has significantly increased its ties with Russia by buying discounted Russian crude and holding joint defence exercises.

Defence spending numbers for China have been increasing; it’s further evidence that they want to challenge the United States as the number one power in the world. The Stockholm International Peace Research Institute (SIPRI) and the International Institute for Strategic Studies (IISS) forecast that defence spending is significantly higher than Chinese government figures. Today, China has the second-largest annual defence budget after the United States.

On the economic front, the U.S. administration is providing significant financial incentives to bring back manufacturing to the United States for key components and technology such as semiconductors. So far, five major chip manufacturers have announced new U.S. factories, totalling new investments of at least US$300 billion.

Recall in our January 2022 Outlook, one of our themes for 2022 was Industrial Renaissance, where we discussed how more key components would be built in the United States.

The United States has also banned exports of certain U.S. semiconductors to China that could be used in advanced weapons technology. China continues to increase its military strength through its naval fleet and advanced weapons such as hypersonic missiles. China’s geopolitical influence continues to expand through regional infrastructure projects and lending to Asian and African countries. According to AidData, since 2013, China’s Belt and Road Initiative granted or loaned over US$843 billion across 13,427 projects in 165 countries. This financing gives China major influence in regional and national politics in various countries to pursue the communist party’s agenda.

Falling interest rates since 1982 had investors used to steady capital gains and income from their bond investments. However, in 2022, investors had a rude awakening as they faced negative double-digit returns for the first time. The combined COVID-related supply chain issues, a booming global economy, and higher oil and food prices due to the Russian invasion led to the highest inflation rate in 40 years. As a result, central banks quickly raised lending rates to slow the economy and tame inflation.

Bonds are usually considered a haven during times of stock market uncertainty. However, last year was a nightmare for bond investors. The FTSE Canada Universe Bond Index ended the year down 12%. Since 1981, there have been only four periods with negative annual returns on bonds: 1994, 1999, 2013, and 2021. Those years saw bonds only down 1% to 5%. Last year’s negative double-digit returns shocked investors, given it was the first time with two consecutive years of bond losses.

Bond mix

Now, investors are asking if they should remain in bonds given that rates are still likely to increase in the short term. Although we expect inflation to peak and rates to stop rising in 2023, the answer depends on your long-term strategic asset mix. Bonds are still an essential part of a balanced portfolio where income is required or used to cushion the volatility of the stock portion of the portfolio. On the positive side, bond yields are now attractive and the highest since 2008, with a yield to maturity of approximately 4.20%.

Our January 2022 Outlook discussed how vital valuation is, especially in a rising interest rate environment. Thus, we were not surprised to see highly valued technology stocks down approximately 30% or more. ECanada’sda’s Shopify was down 73%.

Although technology companies will continue to exist, investing in the sector requires discipline and not getting caught by the media spin on overly optimistic growth expectations. The hype around technology companies has affected the valuation of certain public companies despite the lack of profits.

Twitter’s peak

The lure of low-cost money with unrealistic growth expectations can lead to insane valuations.

For example, Elon Musk paid US$44 billion to make Twitter a private company, a 54% premium to its January stock price, before building his initial 9% position. Elon’s takeover was financed with US$12.5 billion in loans from a syndicate of 10 global banks, with the rest of the US$27 billion (accounting for the 9% he already owned) coming from selling down his stake in Tesla. As of March 30, 2022, Twitter had trailing annualized revenues of US$5.2 billion (with 90% of advertising revenue) and a 12-month trailing net income of US$224 million, with cash of approximately US$6.2 billion and debt of US$5.3 billion.

Let’s say the cash and debt cancel themselves out. So, on the surface, it looks like the takeover valuation was about 8.5 times the current revenue for most people. However, he paid 196 times trailing earnings on a net income basis! Meaning it would take 196 years to earn back the $44 billion paid. No wonder the Twitter board was willing to sue him through the courts to force him to complete the sale!

Crypto Dreams

Over the last two years, many people have asked me about investing in cryptocurrencies, bitcoin mining, or crypto exchanges.

First, I always ask myself how I value these companies, given there are no profits. Disclosure seems opaque; it’s impossible to determine if it creates any tangible economic value. The crypto market reminds me of the Internet bubble 20 years ago, where dotcom companies were valued based on website traffic, crazy ideas, or pure deal-making.

Today, crypto seems to be valued based on similar opaque justifications, such as the number of users and tokens in circulation and speculation that the price will go up. Multiple crypto company bankruptcies and fraud, such as the implosion of crypto exchange FTX, are not a surprise. However, even the most sophisticated investors, such as Caisse de dépôt and the Ontario Teachers’ Pension Plan, were duped. The Caisse invested US$150 million into Celsius Network, which went bankrupt in July, and Ontario Teachers invested US$95 million in FTX, which just filed bankruptcy.

Based on over 30 years in the financial markets, I believe that the combination of low interest rates and the lure of easy money always ends in disaster. Every decade has its excesses and investment frauds as promoters and media hype capture the hearts and minds of investors on the latest ‘new’ thing, and the fear of missing out becomes too great for most investors. Two important ways to prevent investment missteps are to focus on valuation and understand the business. Why risk hard-earned capital if you can’t truly understand the underlying business?

Since the oil price crash of late 2014, energy has been one of the worst-performing sectors globally. Concerns about climate change (carbon emissions, environmental, societal, and governance, the introduction of carbon taxes, etc.), increased regulatory issues, and the cost of new pipeline approvals weighed on the sector. As a result, energy companies under-invested in technology and production since investors did not reward them through higher share prices. The traditional energy sector was out of favour with governments and investors, who instead chose to invest in and promote the renewable sector.

However, in 2022, politicians and global investors saw a significant mindset change. Russia’s invasion of Ukraine brought Europe’s dependence on Russian oil and gas to the forefront. As a result, for most Western countries, a key policy issue has now become energy security and independence. Governments and consumers have awoken that renewable energy is not dependable in all circumstances and that there is not enough to replace all the traditional uses of oil and gas. The demand for oil and gas will continue to grow due to population growth, urbanization, and the growth of emerging market countries.

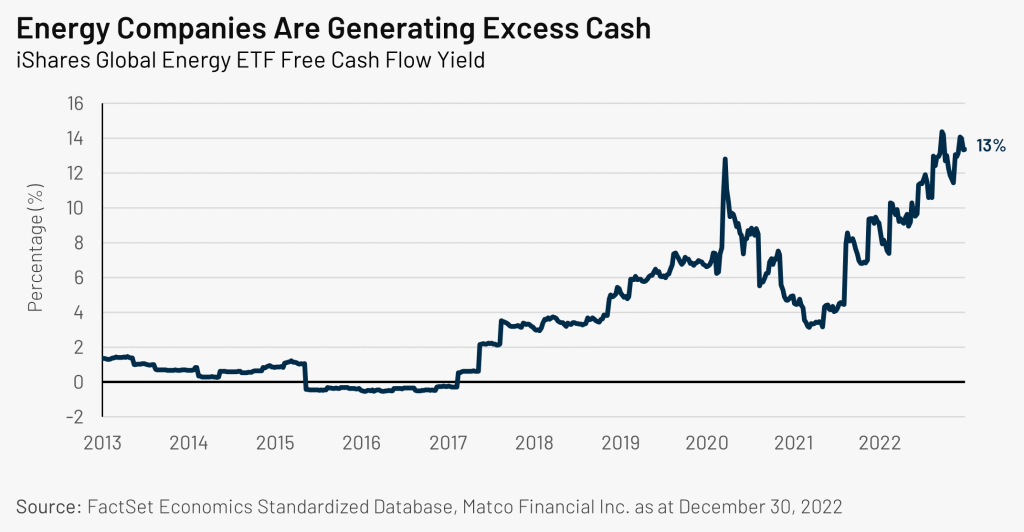

Spinning Cash

As oil and natural gas prices rose globally, energy was the best-performing sector for two consecutive years. Today, energy companies are very capital-disciplined, with many at or being close to debt-free, increasing dividends or buying back their shares. Yet these companies remain relatively inexpensive, trading 4-5 times cash flow with free cash flow yields north of 12%. Although commodity price volatility will continue, energy companies are financially able to handle any future downturn.

Globally, the energy sector has gone from being the poster child of climate change to a vital part of the solution. Today, many energy companies are leading the charge to reduce carbon emissions while building plans for a decades-long energy transition.

Every year, unexpected economic and geopolitical events rattle stock and bond markets. No one can consistently predict what and when these will occur; we can prepare for them by sticking to a disciplined investment process based on valuation and filtering out the media hype about the latest great ‘new’ thing.

Our funds were not immune from last year’s selloff. On average, they were down less than their benchmarks, and our company holdings performed well, with many continuing to increase dividends and buy back shares.

delivered to your inbox once a month