How to benefit from debt consolidation

5 min read • September 6, 2022

5 min read • September 6, 2022

Debt consolidation is a strategy you use when deciding to get yourself debt-free. It combines and merges all the debt you owe into a single, monthly, recurring payment with a fixed interest rate. There are two steps to complete before considering debt consolidation as a repayment method.

Good debt is considered debt that’s on assets. Mortgages and lines of credit fall under good debt. Car loans, credit card balances, payday loans, taxes you owe, and unpaid utility bills are considered bad debts.

Before meeting with a financial advisor about your debt, you will want to know the total amount you owe, the minimum monthly payment, and the interest rate of both good and bad debts.

Reviewing your budget will help you determine how much money you earn, spend, and save by balancing your income with regular expenses. It will provide direction towards how you can reach your financial goals.

Once you have identified your debts and reviewed your budget, you can consider if debt consolidation is beneficial.

When to consider debt consolidation?

Debt consolidation is a good idea when:

When not to consider debt consolidation?

Debt consolidation may not be for you when:

Debt consolidation can help you if you’ve taken steps to assess your financial picture and plan for a different future. Those not ready to change their financial habits can find themselves in more debt after freeing up their credit cards.

Debt Consolidation Requirements

There are specific requirements to determine your eligibility for debt consolidation. Listed requirements vary between lenders, and particular lenders may have less stringent requirements than others. Standard requirements typically include:

Your debt-to-income ratio is calculated by assessing your existing monthly debt payments divided by your monthly income.

What’s the best type of debt to consolidate?

You can consolidate any debt, but certain types, such as unsecured debt, are better suited for debt consolidation due to their higher interest rates and monthly payments. Unsecured debts include car loans, credit card balances, payday loans, taxes you owe, and unpaid utility bills. Out of all these, credit card debt is typically the best to consolidate due to its high-interest rates.

What type of debt consolidation loan is most common?

A Home Equity Line of Credit is one of the most common loan options for debt consolidation, as it typically offers a lower interest rate than other types. It can be used by homeowners who have built up home equity by making monthly mortgage payments or owning the home outright. The loan is considered secured since it uses your home, a physical asset, as collateral.

How does it work?

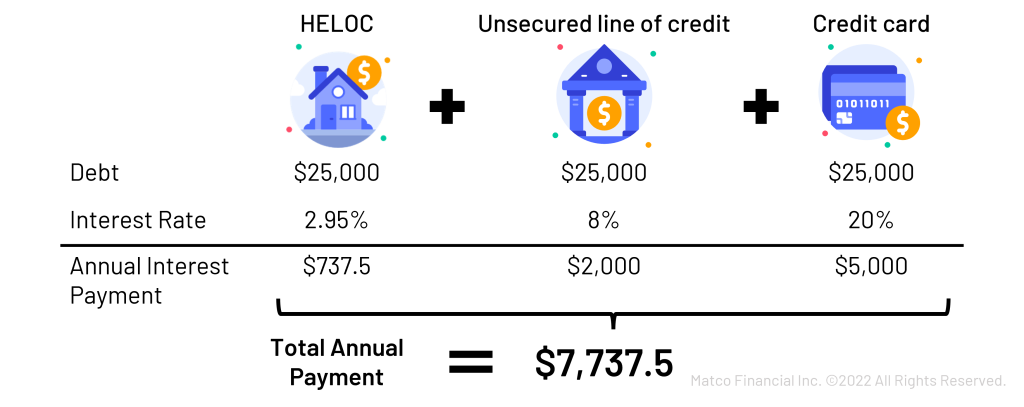

Let’s say you have $25,000 in three different debts, totalling $75,000. Each debt vehicle has a different interest rate with three different annual payment values paid to separate sources.

Your Home Equity Line of Credit has an interest rate of 2.95%, resulting in an annual interest payment of $737.5. Your unsecured line of credit has an interest rate of 8%, equaling an annual interest payment of $2,000. And finally, your Credit Card has an interest rate of 20%, resulting in an annual interest payment of $5,000. These three payments would result in an annual interest payment of $7,737.5 without debt consolidation.

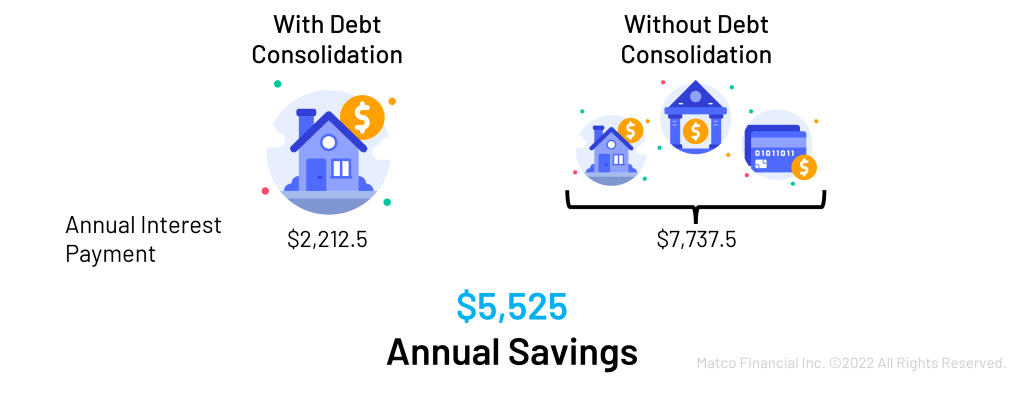

If you consolidate all three by taking out an additional $50,000 on your Home Equity Line of Credit to pay off the other two debts, you would pay $2,212.5 in interest annually. You are saving $5,525 each year in interest payments with debt consolidation.

Investment Loan

An alternative way to pay down debt many people don’t know about requires a financial advisor to help you execute. Investors who hold income-generating investments, such as publicly traded stocks that pay dividends or mutual funds that pay distributions, such as Matco’s mutual funds, can use an investment loan to lower annual interest payments.

What is an investment loan?

An investment loan is when you use your income-generating investment holdings to pay off debt. Investment loans can only be used with a non-registered investment account, which does not include Tax-Free Savings Accounts and RRSPs.

How does it work?

Let’s say you have $100,000 in a non-registered investment account and $100,000 of debt on a line of credit. You can sell the investment account holdings depending on capital gains in the investment account. You then use the $100,000 cash to pay off your line of credit. Once you have paid off the line of credit, you take out a $100,000 investment loan to repurchase the investments. Your interest payments are lower with an investment loan since you can generally claim the investment loan interest payments on your taxes.

When to consider an investment loan?

Investment loans are not suitable for everyone as they require you to have enough income to make loan payments and stay invested for more than ten years. Talking with your financial advisor about whether an investment loan is right for you is crucial. If so, it can be an excellent tool for helping you lower your annual interest payments.

What can you start doing today to eliminate debt?

The two general rules of thumb that you can do on your own are:

Everyone’s debt is unique to them. We provide you with a personalized plan to get more from your debt.

Footnotes:

1Source: Government of Canada website Canadians and their Money: Key Findings from the 2019 Canadian Financial Capability Survey

delivered to your inbox once a month