Magnificent Seven, Valuations, and Matco

March 19, 2024

March 19, 2024

Our role at Matco is to manage our client’s money. You trust us with your hard-earned savings.

— Jason Vincent, President & COO, Co-Founder, Matco FinancialNow that you have stopped working, it’s our job to ensure you aren’t in a position where you have to rejoin the workforce.

In other words, when it comes to managing your money, we make thoughtful investments that present an attractive potential return profile for the level of risk we are taking.

Indexes are more concentrated today than they have been in some time, particularly in the United States. This means the level of diversification provided by an index has declined as the concentration increases.

Enter the Magnificent Seven (Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla) that make up the largest publicly traded businesses in the world as measured by their market capitalizations.

In context, Microsoft has a market capitalization of USD$3.073 trillion; the total market capitalization of Canada is USD$2.497 trillion. Microsoft, one company, is valued at 23% higher than the combined publicly traded businesses on the Toronto Stock Exchange.

Indexes, baskets of securities, are not directly investable; however, exchange-traded funds have allowed investors to put their money in an investment structure that tracks an index.

The top ten holdings in the S&P 500 (which include the magnificent seven) make up 32.3% of the index. In a market capitalization-weighted index, without a cap, the largest companies will make up more of the index as they outgrow the rest of the members.

Diversification is the most effective tool to manage company-specific risks within an index. When index concentration increases, the exposure to those specific company risks increases.

The magnificent seven now trade at an average of 43x their previous year’s earnings. This above-average valuation would suggest some significant growth expectations for the future. After all, there is a reason that they have the market capitalizations that they do – over the last 10 years, they have out-innovated and out-grown their peers.

High expected growth rates and subsequent higher valuations are only justified if the business can meet that expectation. In February of 2022, Telsa traded for USD$290.1 per share or 178x its 2021 earnings. Despite earnings growth over 2022 and 2023, the stock traded at USD$201.9 per share in February of 2024. Tesla didn’t meet the market expectations for growth and the share price declined. The market’s future expected growth expectations have subsequently declined, and its valuation fell to 46.9x last year’s earnings.

The mood of the market swings, sometimes dramatically, throughout time. High expectations for future growth raise stock prices, which the underlying businesses can have a tough time meeting, not because they are bad businesses but because the expectations are unrealistic. It’s a little like my grade eleven English teacher, who would never give out 100% on an essay. As your writing improved, their expectations increased, moving the bar that little notch higher for each assignment.

Investors concerned with the valuation level of some U.S. Securities should consider their options. A part of portfolio management is trimming holdings that have, “crushed it,” meaning those stocks that have surpassed even the best-case scenario for growth. Taking some profits off the table today doesn’t have to mean exiting the market entirely; rather, rebalancing to maintain proper diversification is prudent when the market is greedy.

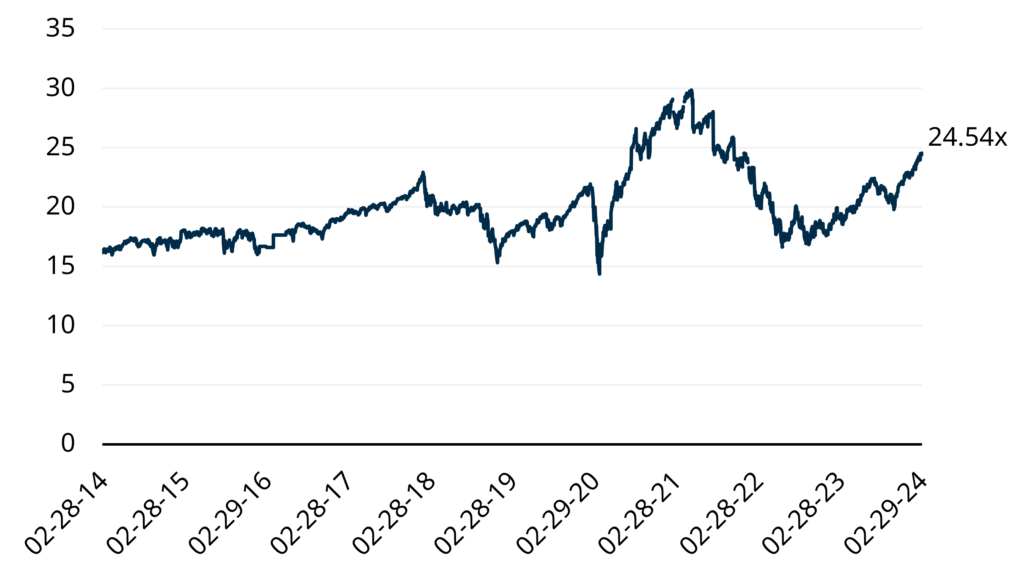

Given our money management role and desire to make thoughtful investments into attractive risk/reward scenarios, our Global Equity Portfolio currently trades at 18x the previous year’s earnings. This is a conservative valuation in comparison to the level of the Magnificent Seven (43x) and S&P 500 (24x). Lofty valuations and high-risk-to-reward scenarios are not what we do—it’s not who we are.

U.S. Market Valuation: Price to Earnings Ratio

Source: Factset, Matco Financial as at March 15, 2024. U.S. Market: SPDR S&P 500 ETF.

The Matco Global Equity Fund does not have a premium valuation because the expected growth rates are more reasonable. A reasonable expected growth rate does not mean poor investment performance. It simply means we are managing risk while investing capital. Over the long term, our goal is to provide attractive rates of return for the level of risk we are taking.

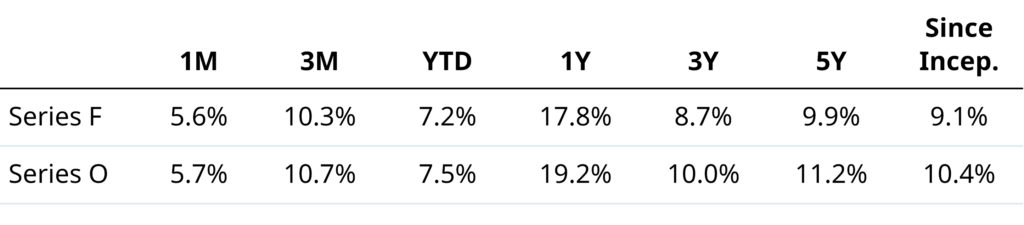

Since its launch in September 2017, The Matco Global Equity Fund has reached a milestone, trading at the highest net asset value per unit in the fund’s history. Something we are proud of and embodies our commitment to a disciplined investment process.

Matco Global Equity Fund Annualized Performance

See disclosure below. Source: Matco Financial, as at February 29, 2024. Inception of the fund is 2017-09-20.

Performance returns for the Matco Mutual Funds are calculated by Matco Financial Inc. These returns are calculated and reported in Canadian dollars and are historical simple returns for the 1-year periods and annualized compounded total returns for periods after 1 year. They include changes in unit value and reinvestment of all distributions and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any security holder that would have reduced returns. Matco Fund returns for Series F units are calculated after management fees and operating expenses have been deducted. Matco Fund returns for the Series O units are calculated after operating expenses have been deducted. Series O unit management fees are charged separately outside of this fund. Series O Management Fees are negotiable based on assets under management. In comparison, the index returns do not incur management fees or operating expenses. Index returns are supplied by a third party. We believe the data to be accurate, however, we cannot guarantee its accuracy.

delivered to your inbox once a month