The Hidden Potential in Bonds

5 minute read • October 3, 2023

5 minute read • October 3, 2023

In a similar fashion, bonds have recently crashed and burned over the last couple of years. Bond performance in 2022 was putrid. With inflation peaking at 8%-9% in North America, central bankers were forced to increase interest rates dramatically, causing turbulence in the performance of bond funds, including those who held bonds within their diversified portfolio.

Today, if one looks closely at the current risk and return setup for bonds versus stocks, perhaps the “Equity Risk Premium” is serenading the bond market as we speak.

On September 25th, the Canadian 10-year interest rate hit 4.0% for the first time since 2007. Similarly, the U.S. 10-year interest rate hit 4.5% for the first time since 2007. With interest rates now much higher and more attractive, coupled with some economic uncertainty, investors are flooding to high-interest savings accounts, GICs, and cash. Bonds are an unpopular opportunity, hiding in plain sight.

We’ve gone through back-to-back years where investors have found reasons to buy something other than bonds. But have bonds truly lost that loving feeling? Often, when investors run from a type of investment, it might be the most suitable time to run towards it. Think about the financial sector post-great financial recession or the energy sector after the COVID-19 pandemic when oil prices dipped to the lowest levels we had seen in decades. Both sectors performed very well after each respective period. The source of pain often becomes the next source of gain.

There’s the anecdotal, but is there any evidence we can point to suggesting that some love may be around the corner for bonds? We’re obsessed with data and analytics in the investment industry, so let’s look.

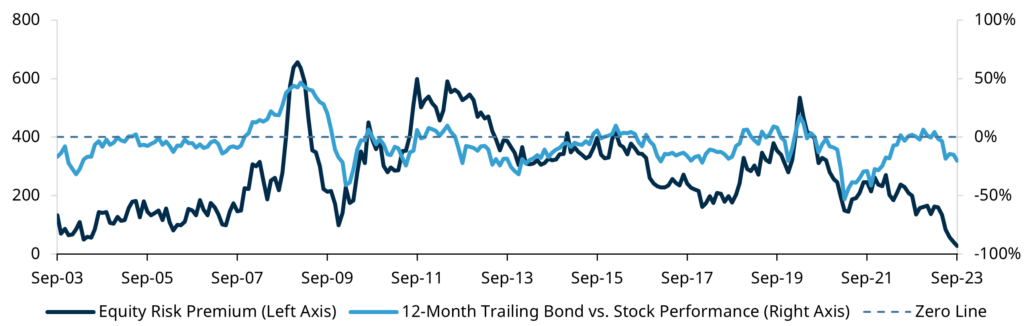

One metric that compares the relative attractiveness between bonds and stocks is the “Equity Risk Premium.” In its most simplistic form, the equity risk premium asks, “As an investor, will I be rewarded enough for the greater amount of risk that stocks represent relative to bonds?”

The equity risk premium is currently at the lowest level we’ve seen in two decades. In 2003 it reached a level of 50 and is now sitting at 28. The numbers may seem arbitrary, but a value above 300 highlights that stocks are more attractive, while a value below 150 highlights that bonds are more attractive.

Lowest level in two decades

Equity Risk Premium

Source: Bloomberg, Matco Financial Inc. as at September 30, 2023

Equity Risk Premium is calculated by taking S&P 500 Current Earnings Yield – 10 Year U.S. Treasury Rate

As asset managers, we make decisions based on return and risk potential. It doesn’t mean we know what will happen in the next 6 or 12 months, but we can identify asymmetry between risk and return to help support our decisions. The equity risk premium is an excellent tool that does just that.

Equity Risk Premium’s track record of identifying stock returns vs. bond returns

12-Month Trailing Bond (U.S. Aggregate Bond Index) vs. Stock Performance (S&P 500 Index)

Source: Bloomberg, Matco Financial Inc. as at September 30, 2023

Equity Risk Premium is calculated by taking S&P 500 Current Earnings Yield minus 10-Year U.S. Treasury Rate

When the equity risk premium reaches a low, stocks have outperformed bonds over the prior twelve months and have become less attractive going forward. Conversely, when the equity risk premium reaches a high, bonds have outperformed stocks over the previous twelve months and are less attractive in the future.

While GIC and high-interest savings accounts have attracted investors in droves, a closer look at the Equity Risk Premium might highlight the opportunity being offered by bonds, hiding in plain sight, that investors might miss over the next 12 to 18 months.

Matco’s Asset Mix Committee adjusts our client portfolio’s investment mix when the tides of risk and return shift in the marketplace. Earlier this year, our Asset Mix committee lowered our stock exposure by 5% and increased our bond exposure by 5% within the Matco Balanced Fund. Within Matco’s Fixed Income Fund, we have steadily increased our exposure to longer-term bonds while interest rates have continued to drift higher. Both active investment decisions are designed to capitalize on the opportunity offered by higher interest rates and the asymmetry surfacing between stocks and bonds.

Now, you may have your objections. If you were to argue that the “Great Balls of Fire” scene with Goose playing the piano is better than the “Lost that Loving Feeling” serenade scene, I’d have a hard time arguing; both are great. Either way, I find myself more focused on how the Equity Risk Premium is serenading the bond market.

If you’d like to discuss the opportunity offered by higher interest rates or Matco’s Fixed Income Fund, please contact your Matco Advisor.

delivered to your inbox once a month